On October 21st, the Korea Chamber of Commerce and Industry conducted a questionnaire survey of 370 South Korean manufacturing companies. The results showed that only 32.4% of companies believed that their technological competitiveness was ahead of that of Chinese companies, 45.4% believed that the gap was “not much,” and another 22.2% admitted that “Chinese companies were ahead.” A similar survey conducted in 2010 showed that nearly 90% of South Korean companies rated themselves as “ahead of Chinese companies.” Furthermore, manufacturing speed, once the hallmark of South Korean manufacturing, has now become “uncommon.” 70% of the companies surveyed speculated that the continued rapid growth of China’s industry over the next three years will lead to a decline in both South Korea’s global market share and sales.

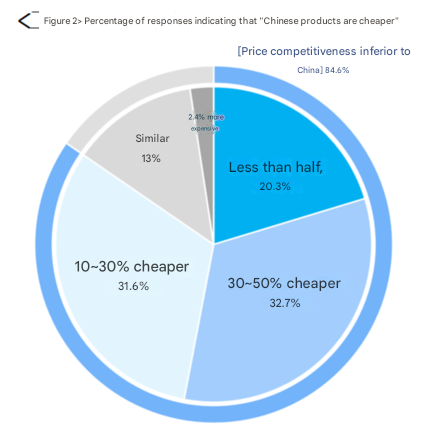

South Korean companies are not only lagging behind in competitiveness, but also struggling to compete on price. A survey showed that 84.6% of South Korean companies surveyed stated that their domestic products are more expensive than Chinese ones, with over half confirming that Chinese products are “over 30% cheaper.” Looking at industry categories , the price gap is particularly pronounced in the display, pharmaceutical and biological, textile, and apparel sectors . An analysis citing data from the United Nations International Trade Center found that Chinese semiconductors are approximately 65% of South Korean semiconductors, while batteries, steel, and textiles and apparel maintain price competitiveness at 73% , 87%, and 75%, respectively.

Driven by government subsidies, corporate cost reductions and efficiency gains, and large-scale production lines, China’s semiconductor industry is increasingly competitive in terms of price . For example, Wolfspeed, a global leader, sells its mainstream 6-inch silicon carbide wafers for $1,500, but Chinese suppliers are now offering prices as low as $500 per wafer or even lower. This, coupled with guaranteed quality compliance at such low prices, is truly astonishing. According to International Data Corporation (IDC), China’s mature chip production capacity will account for approximately 28% of the global market by the end of 2025, and the Semiconductor Industry Association (SIA) has confirmed that this figure could rise to 39% by 2027.

In the steel and textile industries, the key to China’s long-term price competitiveness can be summed up in the ancient Chinese saying, “One force defeats ten skills.” This means that any skill pales in comparison to overwhelming human superiority . Leveraging the vast scale of the Chinese market, its comprehensive industrial sectors, and robust supply chains, a vast workforce has dedicated itself to the steel and textile industries. Combined with the surging technological innovations under the “Smart Manufacturing in China”initiative, these industries have not only overcome technical challenges but also become international standard-setters. This has enabled China’s manufacturing industry to reduce prices even for these “industrial pearls” to rock – bottom prices , securing a commanding market share.

Currently, China’s manufacturing value added accounts for nearly 30% of the global total, and its overall scale has remained the world’s largest for 15 consecutive years. In October 2024, the United Nations Industrial Development Organization released its report, “The Future of Industrialization,”emphasizing that China’s industrial value added accounted for only 6% of the world’s total in 2000, but was projected to rise to 45% by 2030, equivalent to 2.3 times the combined share of the United States, Japan, and Germany.

Analyzing the reasons for being overtaken in just over a decade , the Korea Chamber of Commerce and Industry attributes this to the Chinese government’s investment policies and flexible regulatory measures . By 2025, the “two new” policies — large-scale equipment upgrades and the trade-in of consumer goods— will be expanded across China . The equipment upgrade policy, through financial support and preferential policies, is stimulating demand for equipment upgrades and purchases across various industries , generating a wave of high-quality orders for motors, general components, and other products . The trade-in policy effectively unleashes the consumption potential of the equipment manufacturing industry , fostering positive interaction between consumers and manufacturers and fostering synergistic growth across the industry chain .

Turning to South Korea, July 2, 2021, marked a historic day for the country: the United Nations Conference on Trade and Development officially declared South Korea a developed nation , transitioning from a developing nation to a developed nation. This marks the first time since the conference’s founding in 1964 that a country has achieved this feat. However, over the past four years, impressive growth has turned into a broad-based slowdown. Domestic demand, such as construction investment and private consumption, has recovered slowly, while export growth has slowed rapidly. The momentum of economic growth has weakened, and the decline has been faster than expected. These signs indicate that South Korea’s economic engine is cooling . Meanwhile, South Korea’s tax breaks have failed to benefit businesses. The inverse structure of “larger companies, lower deduction rates”and the awkward policy situation of protracted delays and ultimately “failure” have significantly weakened the competitiveness of the manufacturing industry . In December 2024, the long-awaited “K Chips Act (Amendment to the Special Tax Restriction Act)” by the Korean semiconductor industry once again failed to pass. This bill, hailed as one of South Korea’s key policy tools to maintain its leading position in the global semiconductor competition, failed to materialize.

On October 23rd, the Fourth Plenary Session of the 20th Central Committee of the Communist Party of China concluded. The meeting focused on the 15th Five-Year Plan (2026-2030), outlining development trends for the next five years. This plan will continue the strategic focus of becoming a “manufacturing powerhouse” and promote the upgrading of high-tech manufacturing. Following this meeting, it is expected that China will actively integrate new productivity into its manufacturing sector, aiming to maintain its leadership in the global competition for independent industrial chains and market share.

As traditional technological barriers melt like spring ice, from being “far behind ” to competing on equal terms , and now to being surpassed by more than half , this isn’t the end of the race, but the beginning of a new round of competition and cooperation . On this path, there are no longer eternal leaders, only perpetual change and innovation.

Information contained on this page is provided by an independent third-party content provider. Binary News Network and this Site make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact [email protected]

Comments